文 | Helen

Shortly before starting this article, a timely post from Wayne Kimmel, partner at SeventySix Capital, landed in my inbox: Sovereign wealth funds, private equity firms and global asset managers are allocating meaningful capital to teams, leagues and media rights…Sports is no longer emerging. It’s institutional. And the window for strategic entry is now.

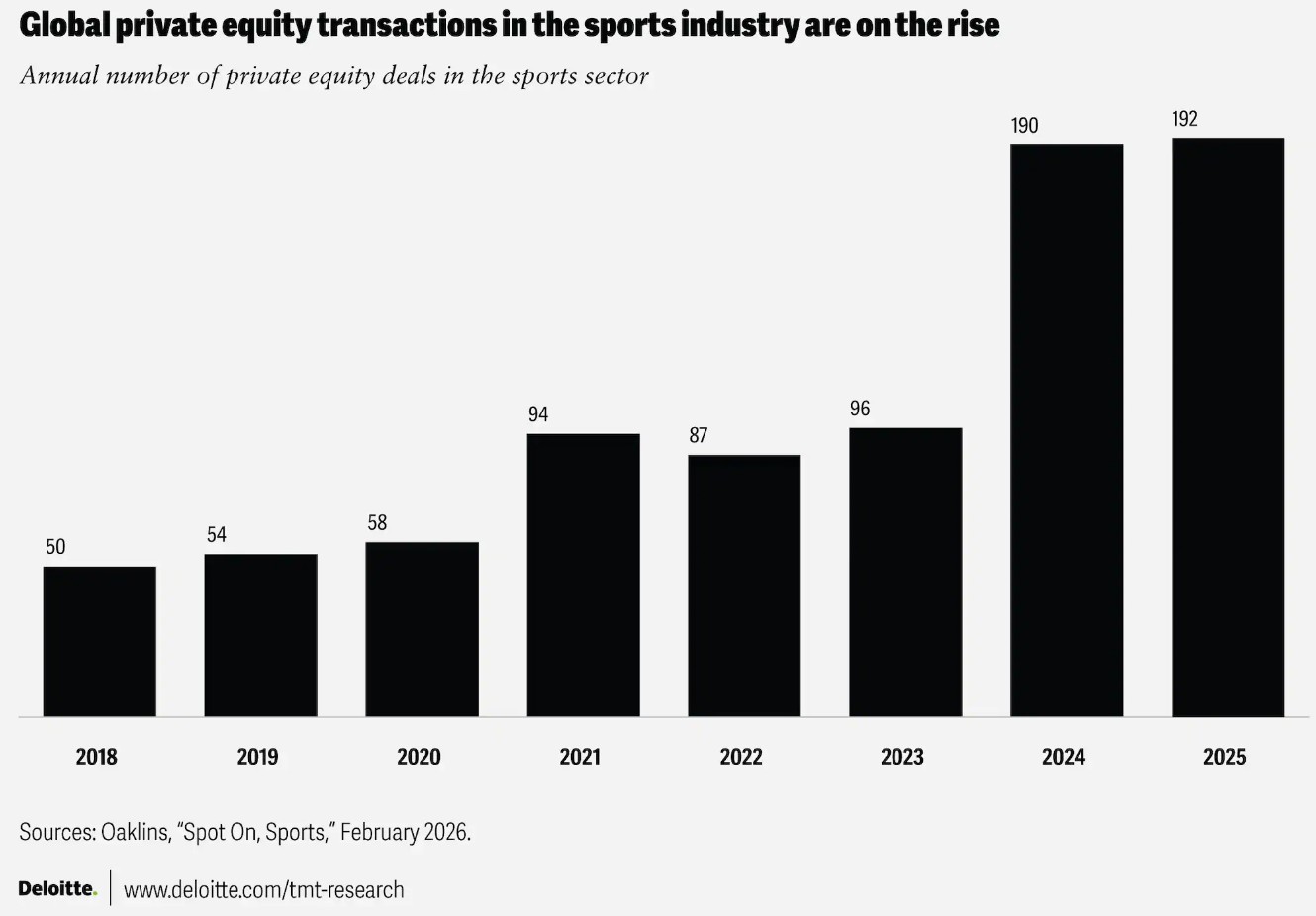

Out of the billionaires' boys' club, elite sports have now attracted a wave of institutional and strategic investors. These include sovereign wealth funds backed by national strategies and substantial resources (i.e. Abu Dhabi United Group and Saudi Arabia's Public Investment Fund), private equity firms with the expertise to orchestrate cross-industry synergies (i.e. CVC Capital Partners and Silver Lake), and major corporations with deep strategic interests (i.e. Red Bull and Adidas). Among these, private equity has demonstrated the most rapid growth. According to Deloitte's 2026 Global Sports Industry Outlook, private equity transations in the sports sector has nearly quadrupled over the past eight-year period.

Global PE Investment in Sport Industry (source: Deloitte)

The Capitalization of the Elite Sports Industry

The capitalization of elite sports is primarily reflected in two dimensions: the financialization of club valuation and the securitization of commercial rights.

First of all, the financialization of valuation is hardly a recent phenomenon. Manchester United's listing on the London Stock Exchange in 1991, for instance, subjected the club to public market pricing. The Glazer family's leveraged buyout then introduced a broader array of financial instruments into the club's operations. Subsequently, the gradual opening of capital structures and the entry of institutional investors have further accelerated this trend. Notable investments include the Abu Dhabi United Group-led City Football Group, which has acquired stakes in multiple city-centric clubs including Manchester City FC, New York City FC, and Melbourne City FC. In 2021, Saudi Arabia's Public Investment Fund acquired an 80% stake in Newcastle United FC. More recently, in 2025, Apollo Global Management agreed to acquire a 55% stake in Atlético de Madrid through a dedicated sports fund vehicle. These value-driven acquisitions extend beyond football. In early 2025, the England and Wales Cricket Board sold majority stakes of the clubs competing in The Hundred to a consortium of Silicon Valley tech entrepreneurs, India-based Sun Group, and US-based Knighthead Capital and many more.

This evolution has brought greater systematization to sport club valuations. Moving beyond total assets and historical performance, valuation models now increasingly incorporate brand value, fan base, predicted sporting performance, and associated potential commercial value.

The second pillar of capitalization lies in the securitization of commercial rights, which future revenue streams, including media rights and commercial sponsorships of clubs, leagues, and even individual athletes, are bundled into tradable assets.

The most emblematic practitioner of this approach is CVC Capital Partners, with its "league-first" strategy. Unlike the club-level equity investments discussed earlier, CVC's model focuses on acquiring a share of commercial rights, including 8.2% of LaLiga's television rights over the next 50 years, and a 13% share of Ligue 1's commercial revenues (through LFP Media) in perpetuity. Following the similar strategy, CVC has also invested in the Six Nations Rugby tournament, the Women's Tennis Association (WTA), and the International Volleyball Federation (FIVB) etc.

Beyond leagues, the IP value of star athletes is also being securitized into saleable assets. A case in point is ABG's acquisition of a 55% stake in DB Ventures (David Beckham's brand management company), effectively securitizing his future endorsement income. Similarly, Excel Sports Management, a sports agency backed by Goldman Sachs, operating by aggregating and commercializing the IP of multiple elites, creates a asset pool that securitizes their future commercial income.

At this stage, the investor's exit logic is no longer tied to the appreciation of a club's equity. Instead, value is unlocked by generating predictable and steadily growing cash flows that form commercial assets which can then be traded in secondary markets.

The influx of capital has revitalized elite sports on multiple fronts. Most basically, it provides liquidity that funds infrastructure modernization, technology adoption, player acquisition, marketing, and youth training. Critically, it has served as a lifeline for clubs facing crises. In 2022, FC Barcelona activated financial levers by monetizing a portion of its future broadcasting revenues through Sixth Street Partners. This move created room for player acquisitions, preventing the club from spiraling into a vicious operational cycle. Similarly, Parma Calcio 1913 , an Italian club facing pandemic-induced losses, had its finances stabilized in time through its acquisition by the Krause Group.

More importantly, strategic capital brings in industry expertise and enables portfolio synergies. Following the acquisition by Liberty Media, Formula 1 leveraged the firm's digital media capabilities to launch documentary content, expanded social media engagement, and successfully rejuvenated its audience demographics. Moreover, Saudi Arabia's Public Investment Fund established SURJ Sporting Investment, investing in streaming platform DAZN and eyeing on fan management tools, to create an integrated ecosystem covering content production to distribution. The Hundred cricket competition, now backed by institutional investors, also aims to leverage its shareholders' footprint in the US and India to enhance international expansion. Additionally, early-stage capital has also increasingly flowed into emerging games and women's competitions, catalyzing their development and diversifying the overall sports ecosystem.

You may have noticed that among the investment cases we've just discussed, the German Bundesliga, one of Europe's top five leagues, appears conspicuously untouched by capital. Does this imply a lack of appeal? Certainly not. In fact, in 2023, the German Football League (DFL) launched a plan to attract private equity investment, which did draw interest from top-tier firms including Blackstone, CVC, EQT, and KKR. However, after protracted negotiations, the plan ultimately fizzled out, due in large part to the fan protest and the constraints imposed by the “50+1” rule.

The Prudent Approach of Germany

Capitalization is not a novel concept for the Bundesliga. As early as 2000, Borussia Dortmund became the first German football club to list on the Frankfurt Stock Exchange (ETR: BVB). Even though its healthy asset-liability structure and robust equity ratio provide ample headroom for both debt and equity financing, the club has refrained from the large-scale external capital that is embraced by many European peers. Instead, Dortmund, on one hand, has adopted a GmbH & Co. KGaA legal structure, ensuring the parent association's ongoing management and voting control post-IPO,on the other hand, has welcomed long-standing sponsors like Evonik and Puma as key shareholders, with patient capital that has underpinned their "investment over dividends" strategy nowadays. As the club's fiscal 2024/25 report indicates, despite stable revenue and healthy free cash flow, Dortmund maintains a “deliberately conservative” financial posture. This prudent approach, so distinct from other leagues, is perhaps most vividly articulated in the words of CEO Carsten Cramer: "We are football clubs. They are football companies."

Because it is a "club," the will of its members and fans outweighs the interests of shareholders. Because it is a "club," long-term financial stability takes precedence over short-term commercial profitability. This philosophy extends beyond Dortmund to a Bundesliga-wide consensus, right reflected in the "50+1" rule. The rule mandates that the "parent club" (the registered association or e.V.) holds at least 50% of the voting rights plus one additional vote (50%+1) in the management company of Bundesliga 1 and 2 clubs, ensuring members retain ultimate control over major decisions, even in the presence of outside investors. The "Fan-centered, community-based" ethos is the cultural backbone of German football. The Bundesliga's prudence toward capitalization, therefore, is not a rejection of capital itself, but a steadfast commitment to preserving the cultural core of the game.

Borusseum Fan Gallery ©Helen

One might reasonably ask: if financing is raised against future commercial rights rather than club ownership, does that preserve the decision-making independence? To a certain extent, yes. However, it does not eliminate the structural impact of revenue-sharing on a club's future financial resources, which otherwise could be allocated to team development, infrastructure investment, or youth training. This fueled opposition to the earlier-mentioned DFL's private equity proposal, and to a large degree, reflects the will of the fans.

As Cramer stated: "Coming from the German market, I'm very sure it is the right approach. The Premier League is more business oriented. People, it looks like, do not complain about it, and therefore the Premier League system is probably the right one for the UK. This system could never be copied and pasted onto the German market, because German habits, German mindsets, and German expectations regarding football are different."

Grounded in the community, German clubs have refrained from importing high-profile sporting executives or overhauling institutional structures with external management. Borussia Dortmund's leadership is homegrown: its former sporting director and current sporting manager are both former players of the club. Centered with fans, the Bundesliga maintains accessible ticket pricing (i.e. an cheapest adult ticket at Dortmund costs €18.50, compared to €60 at Real Madrid and £53 at Manchester City), and the club's 240,000 members retain the absolute power to elect its presidential board. Without a championship title in the past 13 years, the community is continuously growing, and Dortmund still retains the highest average attendance in European football.

If you ever experienced Signal Iduna Park on a drizzling winter night, witnessed 80,000 bodies moving as one, flags cutting through the icy air and a wall of sound rising from an open-air cauldron, felt for ninety minutes that the temperature simply ceases to matter amid that visceral and collective fever, something becomes clear: the hidden logic behind their prudence, and the beating heart of what German football refuses to trade away.

Borussia Dortmund Home Game ©Helen

This prudence grants the Bundesliga the freedom to decide solely in the club's best interest, and the stand to protect what binds it to its fans. Of course, this path has its trade-offs, like the rapid overseas expansion that international capital enables, or the ability to land marquee players at premium prices. On both fronts, the Bundesliga has simply chosen a different way.

For internationalization, the Bundesliga started far later than the Premier League. Yet Borussia Dortmund's trajectory over the past 10 to 15 years tells a compelling story. As Cramer explains: "We have offices in Shanghai, Singapore, and New York doing marketing, PR, caring and concerning on the needs of the supporters, developing sponsoring partnerships, trying to connect us to cultural and political institutions, preparing summer tours and games, organizing setups for the extension of the academy on the ground. In every office, it's a mix of local people and Germans." For Dortmund, internationalization is not merely about rapidly accumulating overseas fans or maximizing media rights value. It is, in Cramer's words, about " time and patience”, about “communicating the club's DNA”, and about “telling the people a story around the world, with some success in sports, with some creativity, with some dynamic and emotion".

Today, over 80 million people consume Dortmund's content across digital platforms, in which more than two-thirds are outside Germany. International fan clubs have grown from a dozen to over 250. And the metrics like media reach on CCTV and ESPN+ and merchandising sales across borders, are continuously rising.

The challenge is even more pronounced when it comes to player transfers, where all leagues compete in the same global market. Here, the financial muscle of Premier League clubs gives them a decisive edge. According to Transfermarkt.de, Premier League clubs spent €4.05 billion on player transfers for the 2025/26 season, far outpacing second-placed Serie A (€1.44 billion) and third-placed Bundesliga (€0.96 billion). When asked about this spending gap and the resulting risk of talent drain, Cramer offered a frank response: "The market is running business by the power of the market…From a purely Dortmund perspective, we decided without any investor, that we just can spend the money we earn by ourselves. That does have certain limits, but if we are happy with "50+1", we can't complain about others who have a different system…We need to be more creative, we need to be faster, we need to be a bit more brave to look for talent. " He then added: "We've built a strong reputation in player development. We are producing superstars season by season, all the big ones, like Haaland, Bellingham, Sancho, Lewandowski…they all have a background in black and yellow."

2025/26 League Transfer Spending and Income (source: Transfermarkt.de)

Similar to Bundesliga, LaLiga on the other hand, while being more accommodating to external capital, has institutionalized its own safeguard: Squad Cost Limit, which sets a maximum amount that a football club can spend on player wages, manager salaries etc. directly based on their revenue. Although this regulatory mechanism places LaLiga also at a structural disadvantage in the transfer market, it has been instrumental in financial stability of Spanish clubs.

The Challenge of Capitalisation

Capitalization unfolds differently across markets, as what unites them is a shared reality: capital has done more than shifts in the financial landscape,it has also subtly reshaped operating models, competitive dynamics, and the very cultural foundations of the industry.

These disruptions have not gone unquestioned. There are persistent debates surrounding the multi-club ownership model and its implications for competitive fairness; questions arising over the optimistic valuation narratives that have diverged from actual revenue-generating capacity, creating further funding shortfalls; concerns that low-revenue sports are being structurally squeezed by capital's preference for scale;and the chaos that increasingly blurred industry boundaries risk steering athlete branding into excessive commercialism and entertainment.

Yet the industry has not responded with inaction. Beyond the structural counterweights discussed earlier, like the “50+1” rule and LaLiga's Squad Cost Limit, concrete regulatory interventions have emerged, such as UEFA's ruling to relegate Crystal Palace that stands as a precedent for preserving competitive integrity, and Borussia Dortmund's continued commitment to its table tennis and handball divisions to support niche sports. Leagues and clubs are constantly evolving, as seen in the recalibrating investor preference in post-pandemic Italy, and rethinking transfer strategy after Mbappé's departure at Paris Saint-Germain. The industry is experimenting, adapting, probing, and balancing, step by step.

However, the greatest challenge that capital poses to the elite sports industry lies in its impact on the industry's cultural foundation. This tension stems largely from the mismatch between capital's short-term exit horizon and the long-term nature of a club's existence. Typically seeking an exit within 5-7 years, capital demands that clubs or leagues generate increased revenues in a rather compressed timeframe.

On one hand, this might push clubs to raise ticket prices as a means of maximizing matchday income. According to The Sports Industry Report 2026 (UK), 67% of fans and 53% of industry insiders believe that attending live sporting events will become a luxury within the next five years. Yet the commercial foundation of this industry is neither its clubs nor its investors, but right its fans and spectators. Losing them, what is left to build upon? As Andreas Preuß, Chairman of the Supervisory Board of the German Table Tennis League, puts it: “Fans are the foundation of any sport, as they give it value. Ensuring their participation is the base for commercial viability…The time is also very different. Young people today have more entertainment options than ever before. Sports are competing with many other industries for their attention. We cannot afford to lose that connection and the emotional bonding with them.”

Table Tennis Bundesliga Game ©Helen

On the other hand, short-term revenue pressures might manifest in leveraged acquisitions of star players, aimed at enhancing commercial appeal and sporting performance. But even setting aside the dubious correlation between star power and sporting success, sacrificing financial stability certainly breeds long-term vulnerability. Where leverage fails to cultivate self-sustaining growth, insolvency is never far behind. Portsmouth FC, FC Girondins de Bordeaux…the cautionary tales are there for the taking. A club does not exist on a 5-7 year horizon. It carries the weight of generations of families whose sense of belonging is passed down through centuries. But once that cultural fabric is torn, it cannot be restored.

"For sport fans, it is not good", observes Rohn Malhotra, founder of SportsTechX and himself both a sports enthusiast and investor, "and from a business perspective, I think there is a valid conversation to be had: are we killing the golden goose? Are we taking too much, too soon? There is a line here...If you ask: are they great opportunities? Are they good investors? Yes, of course. I think the right kind of mindset means the right opportunity. Amazing things can be done. There are great examples of this, but there are a lot of bad examples, too."

Final Thoughts

I keep coming back to something Carsten Cramer said in his interview: " we are not really comparable and competitive to Real Madrid and maybe Manchester City, because they are fighting on a different level. But take notice that we are from Dortmund, which is a small city, an industrial place in Germany, I think we are still able to tell the people a very warm and charming story."

Capital, by nature, is cold. Sport, by contrast, is a human enterprise that has accumulated millennia of cultural warmth. It is my quiet hope that its capitalization might carry with it a measure of that same humanity and a trace of emotion. Let it move a little slower, and find the investors who understand what they are not merely buying, but becoming part of, and the path that leads not to quick returns, but something worth preserving.

快报

快报

根据《网络安全法》实名制要求,请绑定手机号后发表评论